Thought Leadership

View from the Valley: New consumer behavior drives investments and acquisitions

23rd November 2020

When I heard my parents were ordering groceries online for the first time ever, I realized how COVID-19 was changing things. I realized how even laggards in the tech adaption cycle were being forced to adopt digital-first experiences to do work, connect with loved ones and find entertainment. Despite the pandemic being an awful period, tech has found ways to enable people to live their lives. It’s remarkable how COVID-19 has been a change agent and, in many cases, an accelerant of trends that were already in place.

These trends are being fed by a lot of liquidity in the market helping innovative companies to meet these demands; PE has $1.5tn of dry powder, SPACs have raised $40bn so far in 2020, the IPO average valuation on the NASDAQ has doubled compared to last year as investors seek to back these new growth opportunities, and corporates have strong buying power through low interest rates. Not surprisingly, the M&A backlog that built up in the early days of lockdown flooded into the market in Q3, pushing acquisition spending to the second-highest quarterly level in nearly two decades (451 Research).

What are some of the trends impacted by COVID-19? Where are investors and buyers putting their money? And what’s the outlook for the future?

Software connecting people

Companies that have played an important role in connecting people during periods of lockdown have done well. Companies like Microsoft, ServiceNow, and Zoom are leading the charge and their stock has soared to new heights.

Companies that support the remote management of people have also done well. Remote, an online platform that provides human resources services for companies that have adopted remote working, raised $35mn in its Series A funding round. The company says its customer base is doubling monthly.

COVID-19 has also spawned the emergence of new product categories, such as virtual events. One example here is UK based Hopin who recently raised $125mn at a $2.1bn valuation as virtual events become the new norm.

New innovations in the market involve AR and VR to render workspace in 3D to collaborate in real time. Environments where we collaborate as avatars and objects and react to our physical touch are going to be the areas where investors will focus. Some innovative companies include Labster, a Copenhagen-based startup, that secured $9mn in equity venture funding from GGV, Owl Ventures, Balderton and Northzone. Another company, Digital Surgery was acquired by Medtronic in February 2020 and whose Touch Surgery app provides AR and VR simulations for training surgeons and students outside the operation room.

Tech-enabled services delivering essentials to consumers

On election night, the most ordered takeout food was french fries, followed by chicken fingers and cheeseburgers, according to DoorDash, the food delivery company. Not only on election night but on every other night too, it seems, app-based ordering and delivery of food has seen massive growth. DoorDash revenues reflect the explosion in demand for delivery. Last year, DoorDash generated $885mn in revenue. During the first nine months of 2020, revenue more than doubled that to $1.9bn – that’s 226% growth this year so far. All this culminated in DoorDash recently releasing its filing to go public.

People of all ages are getting more groceries delivered than ever before. This change in consumer behavior is causing tech giants like Uber to pivot its focus to grocery delivery as a natural step for the company to expand its business. In fact, Uber is said to have recently acquired Cornershop, a grocery delivery startup, that started serving the Latin American market and recently shifted to offer service in Toronto, its first North American city. Other players in this space include Instacart, that surged to a $17.7bn valuation, becoming the most valuable venture-backed food delivery company in the US, according to PitchBook data. The company got a $17.7bn valuation in a $200mn fundraising round last month but it is reportedly aiming for a $30bn valuation in its IPO which could come early next year.

To keep up with demand, online-only restaurants will emerge fundamentally changing the nature of the industry – a trillion-dollar sector. We’ll also see reconstitution of the infrastructure with cloud kitchens, replacing many small businesses driving the industry today. Unfortunately at the cost of restaurants closing and employees losing their jobs, platform mediated businesses will be the winners.

Online entertainment delighting consumers

When not able to meet face-to-face or go the gym, consumers flocked to the virtual world of gaming, online workouts, and online learning to have fun, stay fit and continue education.

Many consumers discovered mobile gaming for the first time and continue to return to it. This is shown by increased engagement levels and monetization for games companies. In the first and third quarters of 2020, investment in gaming surged alongside some big acquisitions. In September 2020, Microsoft acquired ZeniMax, a media company connecting game developers, artists, designers, programmers, and talents to create entertainment content, for $7.5bn. Earlier this month, Take-Two Interactive Software Inc., the company behind popular video games including Grand Theft Auto and NBA 2K, agreed to buy the British developer Codemasters Group Holdings Plc in a cash-and-stock deal valued at about £726 mn ($956mn).

Global funding for gaming companies so far this year has already blown past 2019’s totals. VC and PE investors have injected $5.9bn across 332 deals, according to PitchBook data. In 2019, the total funding figure was $3.2bn over 531 deals. Scopely, a creator and publisher of mobile games, has raised a $340mn Series E from Wellington Management, BlackRock and Battery Ventures. With the new funding, the company has reportedly almost doubled its valuation to $3.3bn. Zynga reports record revenue and strong user growth, however, while still losing $122mn.

With people of all ages flocking to online classes for fitness, cycling and yoga, we saw companies like Patreon, a subscription website that enables fans to pay instructors for their work raise $90mn from New Enterprise Associates, the Maryland-based venture capital firm, and Boston’s Wellington Management. It’s now valued at $1.2bn. The site makes it easy for, say Yoga teachers like me, to charge for and provide access to classes. In the past the physical Yoga studios would take care of this through MindBody, class scheduling and payment software.

Online cloud-based learning and education tools also continue to see a surge of interest boosted by major changes in work and learning practices in the midst of the pandemic. Udacity, which provides online learning courses was unprofitable prior to COVID-19 and recently secured $75mn in debt reported Q3 bookings up by 120% year-over-year. Beijing based Yuanfudao, a live tutoring platform, raised another $1bn at a $15.5bn valuation, the highest valuation for an edtech company. The round was led by DST Global, which also invested earlier this year in India’s BYJU’S, a K-12 learning app. Yuanfudao has raised $3.2bn in total this year so far.

Consumers preferring contactless payments

Venmo is all the rage here in SF. Vendors from hairdressers to fitness trainers understand that no one wants to handle cash and as a result person-to-person and digital wallet services like Venmo, PayPal, Venmo and Zelle have benefitted. The use of these products is no longer being driven by digital natives and millennials but instead new populations that have found comfort with digital and will adapt more financial services. Covid-19 has accelerated the shift away from cash with contactless and digital payments.

Between the first and third quarters of 2020, investment in payments surged as funding steadily rose. Payments companies raised almost $4bn in Q3’20 across 109 deals, a QoQ increase of 4% and 5%, respectively. Notably, mega-rounds accounted for 65% of total funding to the space in the quarter. On August 25, Ant Group (formerly known as Ant Financial), the parent of super app Alipay, attempted to IPO in Shanghai and Hong KongThe IPO, which was destined to be the largest IPO of all time at $37bn, was put on ice from Chinese regulators pending further investigation.

Visa and Mastercard reported 40% year over-year global growth for tap-to-pay or contactless transactions. Mollie, a Dutch payments services provider (PSP) that builds payment products, commerce services, and APIs that let users accept online and mobile payments, raised $106mn Series B from TCV and was valued at $1bn.

The FAMGA companies were also active in fintech this quarter; Facebook, Apple, Microsoft, Google, and Amazon completed patent approvals, partnerships, and investment activity. Notable was Apple’s acquisition of Canada-based mobile payments company Mobeewave for $100mn. Google participated in a $20mn seed round to mobile-based investment advisory app Pingan Huixin. Amazon participated in a $60mn Series D round to digital insurance provider Acko General Insurance.

Consumers moving to home drug delivery and online doctor visits

With consumers electing to have prescriptions delivered to their door and patients seeking alternatives to the physical trips to a doctor’s office when possible, we’re seeing the digital transformation of medical practices and hospitals. In France Doctolib saw the number of video conferences on their platform grow from 100,000 in the 13 months before lockdown to 4.6mn today.

Not surprising, telehealth funding skyrocketed to reach $2.8bn in Q3’20 across 162 deals, setting an all-time high in both deals and dollars. Five companies became unicorns (private market valuation of $1B+) in Q3’20. Lyra Health, VillageMD, and Ro offer telehealth services, while China-based Waterdrop provides an insurance marketplace for high bills and Sema4’s platform offers genetic screening services. On the M&A front, in July 2020, Microsoft acquired Orions Systems, a provider of digital video and data management solutions for organizations in the health care industry.

GoodRx which operates a telemedicine site and online marketplace for discounts on prescription drugs, went public last month in a smash debut with a valuation of $19bn. Other successes include OneMedical, Amwell and who also racked up high valuations. To rapidly adjust to the significantly increased levels of demand in online consumer health, this year Swiss based online pharmacy Zur Rose Group, advised by our strategic partners Acxit Capital Partners, has raised a total of CHF390mn and acquired the mail-order activities of the online pharmacy Apotal and also TeleClinic, Germany’s leading telemedicine provider.

Consumers going online at unprecedented levels

Innovation comes out of all crises. In WW2, as men were fighting, women entered the workforce, this trend persisted after the war and was an important economic change. Returning veterans who wanted a more easeful life moved out of cities spawning the suburbs, and the result was the growth of the car industry.

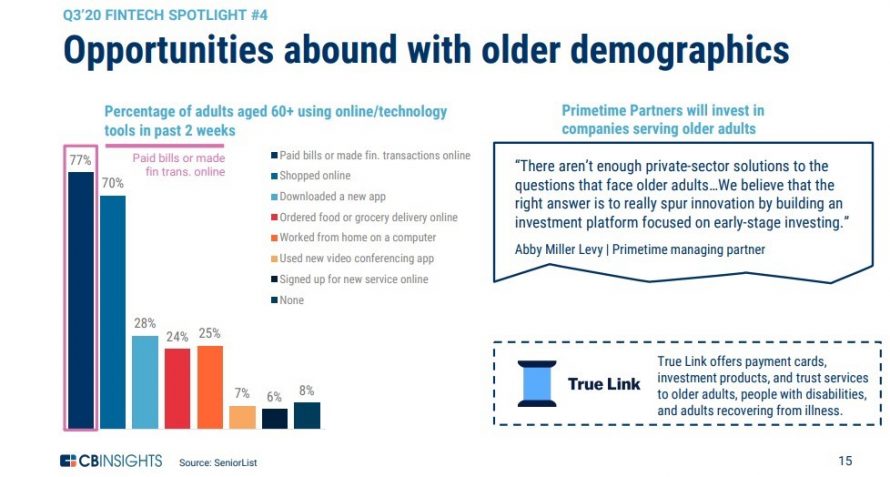

While we’re still navigating the tailwinds of COVID-19 and time will tell what the resilient trends will be, some trends are already visible. One trend that is already apparent is the digitization of newer populations, and in particular, the older generation. The image below shows the shift in behavior.

Outlook for investors and buyers

The level of investment and M&A activity in these tech sectors will depend on how the economy recovers. In the US things certainly feel more optimistic in terms of stability around the election of President-Elect Biden and the positive vaccine news. There’s also a view that a Republican-controlled U.S. Senate would restrain Biden’s most interventionist policies. This dynamic can be quite conducive to doing deals, because it provides stability.

Even if interest rates do go up a bit, they will be maintained by monetary policy which will keep the cost of borrowing money low for investors. Historically, we haven’t seen such global fiscal policy ($2tn pumped into the economies around the world by central banks) being applied, so it might make sense to feel the stock market will go higher and that this is reasonable.

On the downside, it’s likely the stimulus relief in the US will be moderate with the news of the vaccine and the third wave of COVID-19 which may lead to more lockdowns. It all depends on the magnitude of these factors.

What we can bank on is that the new behaviors and trends birthed by COVID-19 will crystallize as we move into 2021 and beyond. And there’s no doubt these trends will spawn new innovations for investors and strategics to finance. Only time will tell what the greater more impactful and resilient impact of COVID-19 on tech will be.