Demystifying M&A

Why your exit proceeds may be lower (or higher) than the headline price

25th March 2026

Many founders will sign a letter of intent with a headline price of £xmn, and that’s what they think they will get. But then at completion, they discover that the actual proceeds are materially lower, sometimes by millions, and this can be a very unpleasant surprise.

The discrepancy is the result of how the valuation you’ve agreed converts into what the buyer actually pays. A £100mn Enterprise Value deal can easily become proceeds of £90mn (or could be £110mn) once cash, debt, working capital and other items are taken into consideration.

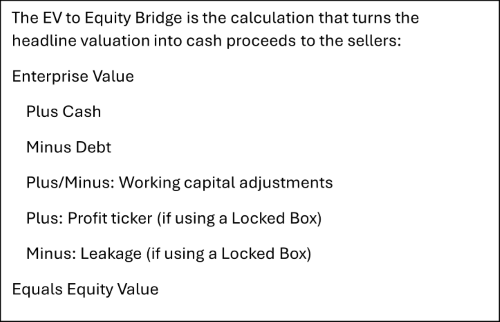

The EV to Equity Bridge

How you get from headline price to actual proceeds is represented in the deal by a mechanism called the EV to Equity Bridge. It is determined by negotiation of several key items, which can all add up to quite a lot of money.

In your letter of intent (LOI), you will agree an Enterprise Value (EV) based on acquiring the business on a cash-free/debt-free basis and with a normalised level of working capital. Then in order to work out what you will actually receive (the Equity Value), you need to make a number of adjustments:

Cash-free/debt-free means that any excess cash in the business is added to the Enterprise Value and any debt (or debt-like items) is subtracted. However classifications of cash/debt are not automatic. Effectively negotiated they can materially affect proceeds.

- What is cash? This seems simple, but for example a buyer will push for “trapped cash” located in jurisdictions where it is hard to repatriate the money to be excluded

- What is debt e.g. tax due for periods prior to completion or back pay/accrued bonuses are considered debt

- Contentious areas include things like whether or not deferred revenue is debt, especially for SaaS businesses where the cash may have been received pre-close (if the customer pays in advance) but the buyer has the obligation (and the costs) to deliver the product post close. Is it a debt, or is it working capital?

Normalised working capital can be a big swing factor, especially if your business is seasonal. You have to leave a “normal” amount of working capital in the business in order to meet day to day obligations. But there is a huge amount of subjectivity in how you “normalise” working capital, and over what period, e.g. long look back periods often disadvantage fast growing tech companies.

Locked Box vs Completion Accounts

Most M&A deals in Europe are done on the basis of a Locked Box. This involves agreeing a date prior to completion on which the balance sheet will be “locked” and effectively the deal is done from an economic perspective. All balance sheet items are diligenced by the buyer as of that date, and any balance sheet adjustments are negotiated and agreed prior to completion. As a seller this is a major advantage in terms of reduction in risk and certainty of ultimate proceeds.

Usually with a Locked Box a profit ticker is also agreed. This is the daily profit generated by the business based on actual performance averaged over a period of time. A sum equal to the profit ticker times the number of days between the Locked Box date and completion is added to the EV to Equity Bridge to cover the additional value generated in that period.

The seller agrees to operate the business between the Locked Box date and the completion date in the normal course of business, and if any payments are made in that period which are not normal course, they are considered “Leakage” and must be deducted.

Note that US deals often do not use a Locked Box but use Completion Accounts, whereby the balance sheet is not finalised until the day of Completion, and there is a post completion “true up” based on the actual balance sheet on the day.

The negotiation of the EV to Equity Bridge is an area where founders can unknowingly give up significant value. Early preparation, clear positioning and robust negotiation can materially change outcomes. Talk to us to find out how we help our clients protect their proceeds.